What 2026–2027’s Economic Reality Means for Europe’s Food Industry — Segment by Segment

Europe is heading into 2026–2027 with modest growth and near-target inflation — but that doesn’t automatically mean an “easy” trading environment for food.

The European Commission expects EU GDP growth around ~1.4% in 2026 and ~1.5% in 2027; inflation sits roughly ~2%.

The ECB has a similar euro-area view: GDP ~1.2% (2026), ~1.4% (2027), with inflation around/slightly below 2%.

The IMF also sees a global soft-landing vibe continuing into 2027 (with Europe broadly in that “steady but not booming” camp).

So yes: the macro picture is calmer than 2022–2024. But the food industry is still operating in a world of value-first consumers, policy-driven cost shocks, and climate volatility.

Below is the practical impact — by segment.

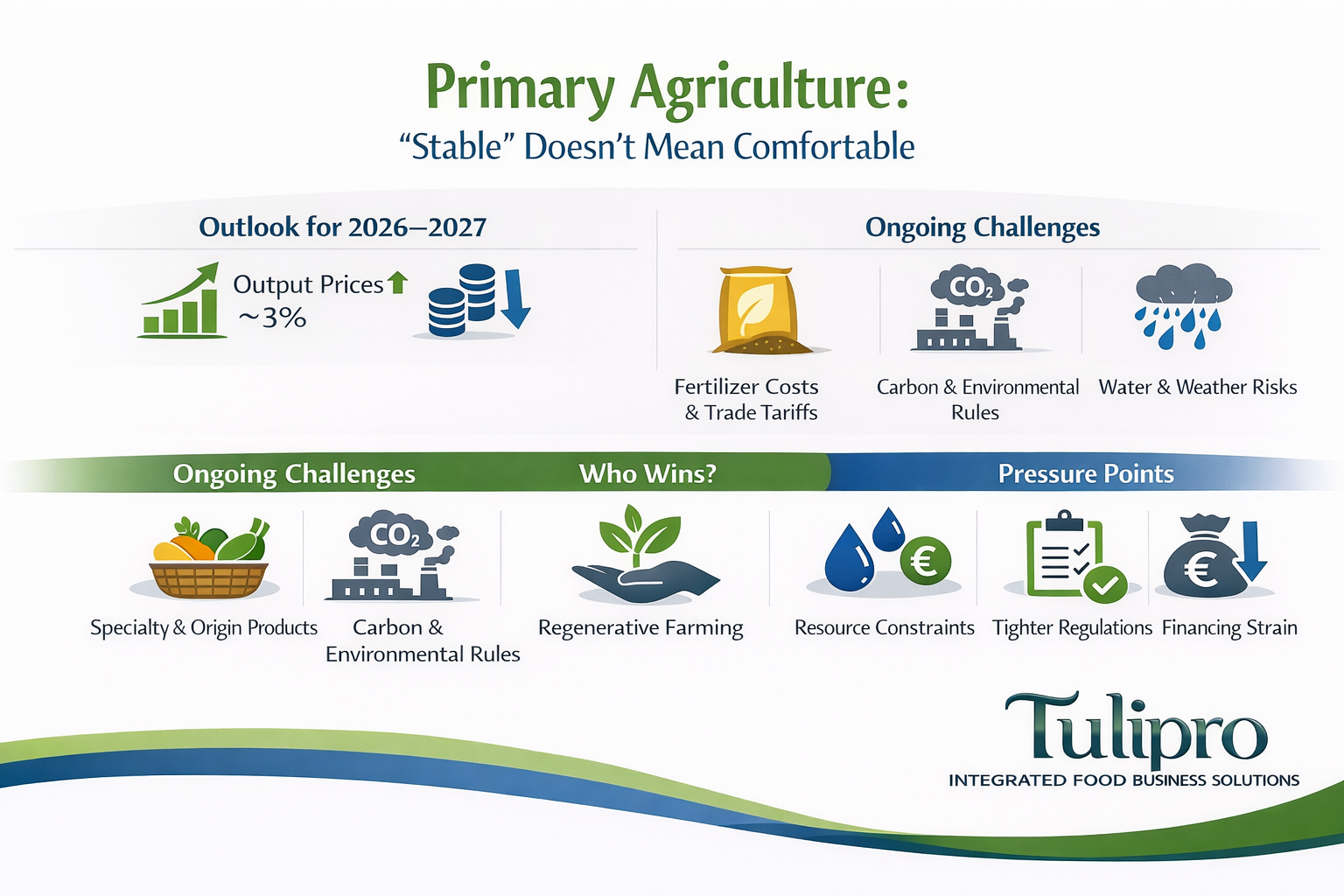

1) Primary agriculture: “stable” doesn’t mean comfortable

What changes in 2026–2027: price stability improves a bit, but margin pressure remains structural.

EU data suggest agricultural output prices rose ~3% in 2025, while input prices rose <1% — a sign of stabilisation vs the worst inflation spikes.

But inputs are policy- and trade-exposed, especially fertilizers (EU tariffs on Russian fertilizer imports and carbon-related border policies can feed back into costs).

Winners: specialty, quality-differentiated supply (origin, welfare, regenerative claims), and growers with contracting power.

Pressure points: water/weather risk, tightening environmental requirements, and financing/capex constraints.

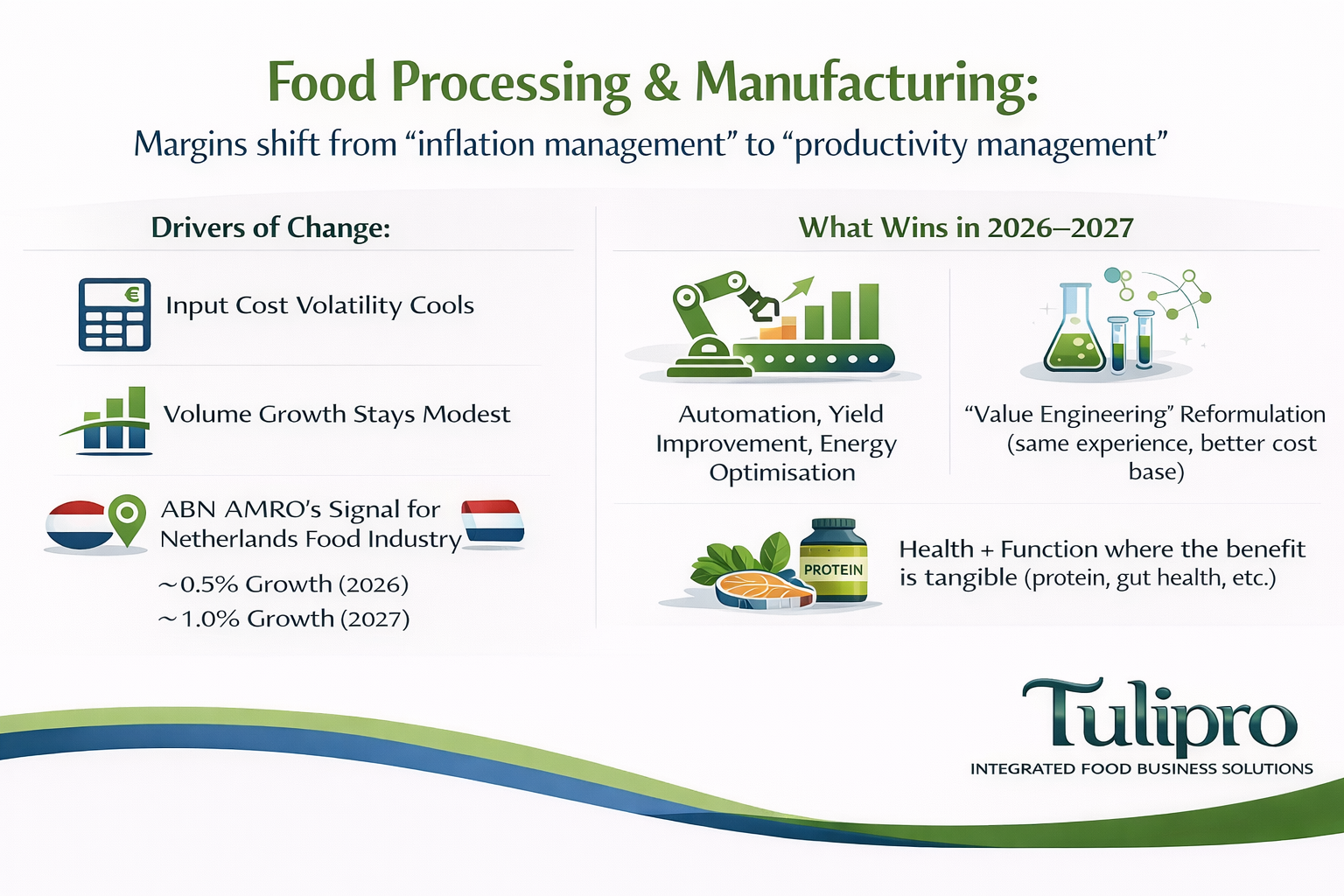

2) Food processing & manufacturing: margins shift from “inflation management” to “productivity management”

What changes: input cost volatility cools, but volume growth stays modest.

A useful signal from ABN AMRO: for the Netherlands, food industry growth is expected around ~0.5% in 2026 and ~1% in 2027 (not Europe-wide, but directionally consistent with “low growth”).

With inflation nearer target, the battlefield becomes: efficiency + mix + innovation that justifies price.

What wins in 2026–2027

Automation, yield improvement, energy optimisation

“Value engineering” reformulation (same experience, better cost base)

Health + function where the benefit is tangible (protein, gut health, etc.)

3) Retail & grocery: private label keeps taking shelf space (and mindshare)

Even if headline inflation normalises, shoppers won’t instantly “snap back” to old habits.

Private label in major European markets is now ~42% of CPG value sales across EU6.

Circana also points to ~44% private label value in European F&B, with growth supported by promotion and mix.

Inflation has cooled at the macro level (euro area inflation 1.9% in Dec 2025), but value behaviour remains sticky.

Implication for brands: you don’t just “compete on price.” You compete on:

differentiation consumers can feel (taste, convenience, function)

availability + execution

and clearer pack-level value communication

4) Foodservice & hospitality: demand is selective; digital is structural

Foodservice is recovering, but unevenly — and consumers are choosier.

Some countries still show visits below 2019, while markets like Germany are expected to see modest visit growth into 2026, helped by digital ordering/delivery adoption.

Industry commentary for 2026 emphasizes a tougher operating environment (cost volatility, labour pressures) and the need for sharper execution.

Who’s most exposed: mid-market operators without a strong value story or a distinct experience.

Who holds up better: QSR/fast casual with strong throughput, and premium venues with “occasion value.”

5) Ingredients: growth concentrates in “function + reformulation tools”

This segment mirrors two mega-drivers:

health/function, and

cost-down reformulation (while maintaining label simplicity).

In European innovation pipelines, the most resilient ingredient areas are tied to:

digestive wellness / gut health,

protein quality,

stress/mental wellbeing,

cleaner labels / familiarity of inputs.

Under pressure: undifferentiated bulk ingredients where procurement squeezes margins hardest and substitution is easy.

6) Exports & trade: “specialised beats commoditised,” and trade policy is the wild card

The baseline view from the ECB is improving foreign demand, but with ongoing competitiveness issues and a drag from trade uncertainty/tariffs.

What that means in practice

Specialised products (premium dairy, branded specialties, functional ingredients) tend to be more defensible.

Bulk exporters face tougher price competition and bigger FX sensitivity.

What I’d watch most closely in 2026–2027

Private label further premiumising (not just “cheap”)

Capex discipline + productivity projects in manufacturing

Fertilizer and energy policy effects feeding into farmgate costs

Foodservice traffic vs. ticket (value menus, bundles, channel mix)

Health-forward innovation with proof, not vague claims